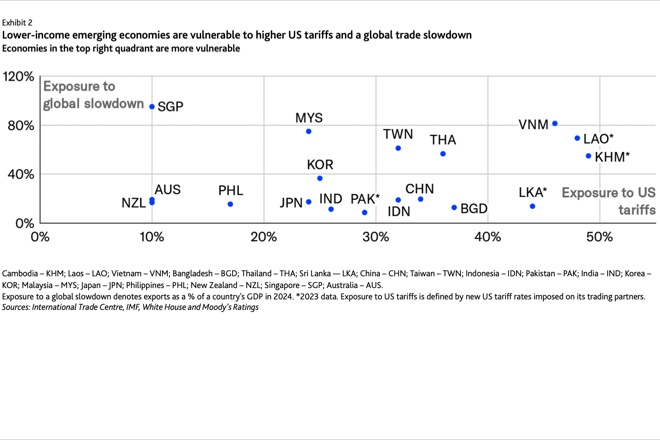

Frontier markets such as Sri Lanka, Pakistan (Caa2 positive) and Bangladesh, which do not have the capacity to import as much from the US and whose current account balances are relatively fragile, could see a worsening of their broader external positions that will potentially weigh further on the outlook for economic growth, according to the latest report by Moody's Ratings.

The new tariffs on APAC economies are more draconian than market expectations and will be credit negative for the region, but with some differentiation.

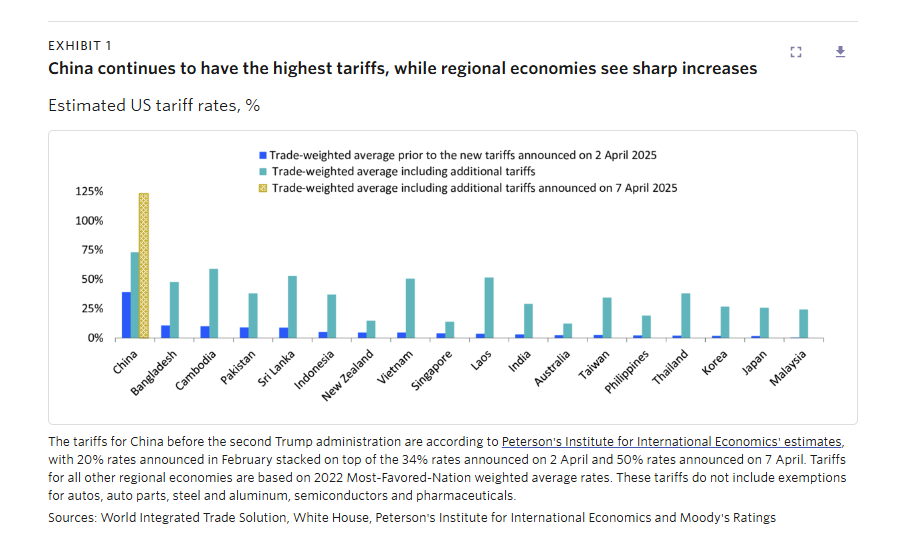

Some of the highest tariffs (>30%) were applied to a number of economies in the ASEAN bloc, such as Cambodia (B2 stable), Laos (Caa3 stable), Vietnam (Ba2 stable), Thailand (Baa1 stable) and Indonesia (Baa2 stable), as well as South Asian economies such as Bangladesh (B2 negative) and Sri Lanka (Caa1 stable).

The new tariffs will hurt the 'China+1' strategy, and an acceleration in supply chain diversification away from China is more uncertain at this stage. However, APAC economies may still be incentivized to deepen trade and investment ties intra-regionally

Highlights

- Lower-tariff countries like Malaysia, India, and the Philippines might gain market share through trade triangulation to serve the US market.

- Countries with large domestic markets, such as India, may benefit from production shifts in the long term.

- Higher tariffs will affect global trade, reduce regional export demand, and lower business confidence, leading to decreased investment in APAC.

- APAC economies face both direct and indirect exposure to higher US tariffs. Vietnam, Cambodia, Thailand, and Taiwan have high direct exposure, while Pakistan and Bangladesh's exposure is concentrated in specific sectors.

- Countries will also be indirectly impacted through value-added contributions to other nations' exports, with significant links to connector economies like Vietnam, Singapore, and Malaysia.

Important Takeaways

China has announced a 34% duty on all US imports starting April 10th, matching the US tariffs imposed on April 2nd. This escalation in Sino-US trade tensions poses significant risks to the region's economic outlook.

Most APAC countries are expected to negotiate rather than retaliate against the US tariffs. Strategies include seeking talks, establishing bilateral trade agreements, or increasing purchases of US goods. However, APAC will still face significantly higher tariffs overall.Currency depreciation, financial market volatility, and heightened refinancing risks for non-investment grade issuers are potential concerns. Some governments are implementing measures to support their economies. For example, Japan is offering loan support for SMEs in the auto supply chain, and China's sovereign fund is stabilizing the stock market.Governments in the region are likely to enhance cooperation and promote substitution of US exports with other markets. Central banks may ease monetary policy to support growth. Fiscal responses could weigh on sovereign credit but may be constrained by higher debt burdens from the pandemic.The impact on banks is credit negative, with greater effects on banks in Vietnam, Thailand, and Bangladesh due to their higher dependence on US exports.