The Sri Lankan government’s proposal for treatment of domestic debt marks a significant step towards resolving uncertainties around the impact of the sovereign’s debt restructuring on the local banking sector, says Fitch Ratings.

Full statement

The Sri Lankan government’s proposal for treatment of domestic debt marks a significant step towards resolving uncertainties around the impact of the sovereign’s debt restructuring on the local banking sector, but complications may arise from a number of factors, says Fitch Ratings.

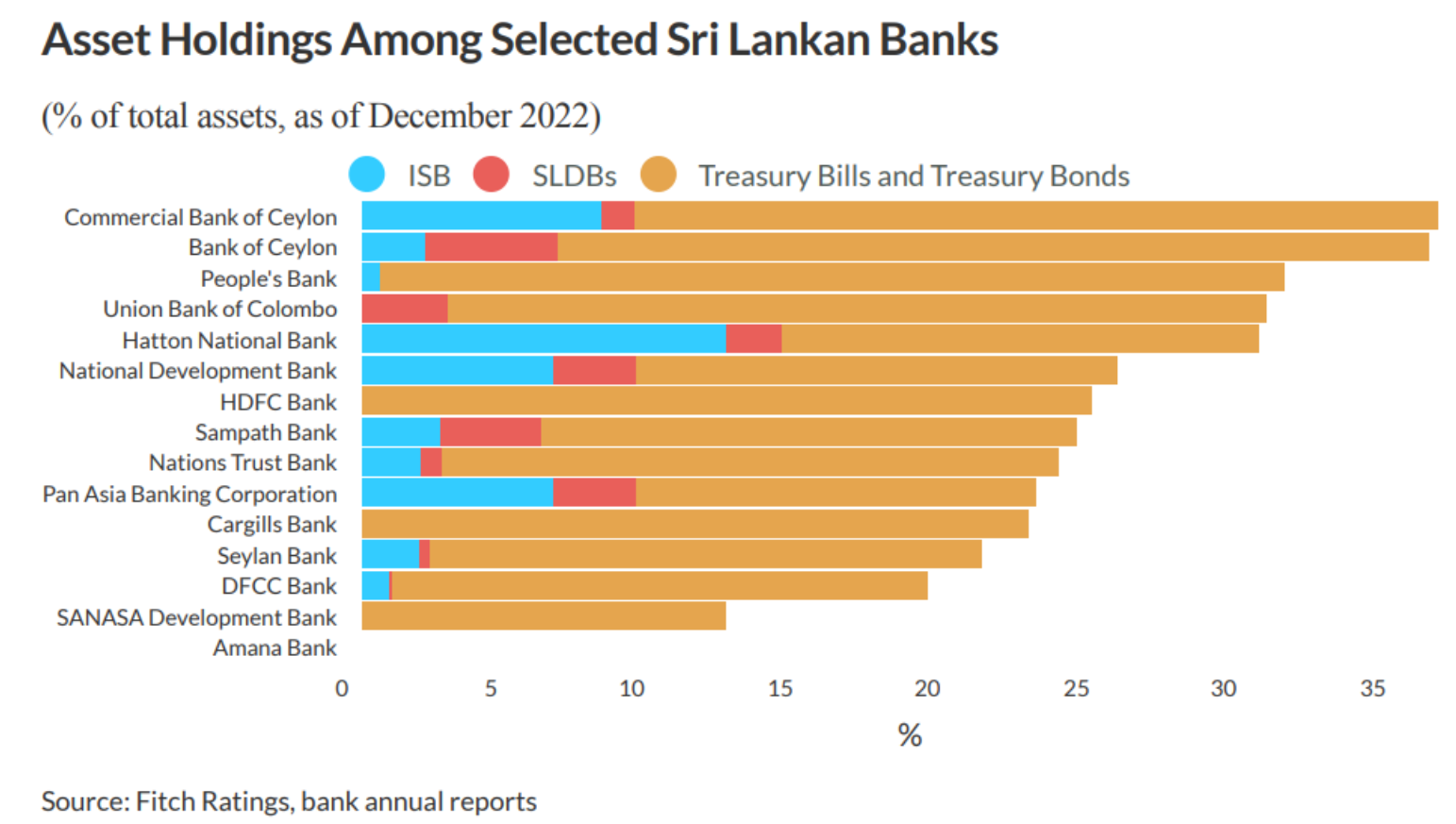

The proposal excludes banks’ holdings of Sri Lankan rupee-denominated treasury securities, which will alleviate some of the pressure on their already stressed capital positions from weakening loan quality and the rupee’s depreciation. Fitch’s base case did not expect treasury bills held by banks to be subject to restructuring, but assumed banks’ treasury-bond holdings would be. Bank holdings of Sri Lanka Development Bonds (SLDBs), which are foreign-currency denominated but governed by local law, will be affected, as we had anticipated, and we still expect an impact on international sovereign bonds (ISBs) as well. However, these together account for only about 5.5% of banks’ combined assets, a much smaller share than treasury securities (26.4% for Fitch-rated domestic banks). The proposal also includes a restructuring of foreign-currency bank loans to the government (less than 1% of combined assets for Fitch-rated banks), though without detailed plans.

The government has outlined three treatment options for SLDBs. We expect banks will generally opt for the choice involving conversion of such debt into local currency-denominated instruments; banks have so far opted to convert maturing SLDBs to rupee-denominated treasury bonds since the announcement of suspension of foreign debt servicing in April 2022.

Provisioning should help to moderate the hit to bank capital from the debt treatment. Fitch-rated Sri Lankan banks have already made provisions of 35% or higher for ISBs, with SLDBs being subject to lower provisioning due to the possibility of obtaining rupee-denominated treasuries.

Nonetheless, worsening impaired loans (end-May 2023: 13.3% of system loans, from 1Q22: 8.4%) in line with the economic stress associated with the sovereign default and the unwinding of forbearance provided during the Covid-19 pandemic are already exerting pressure on banks’ thin capital buffers.

We do not believe a restructuring of the sovereign’s local-currency obligations is likely to trigger a loss of depositor confidence in the banking system, based on the proposed plans. However, funding stress remains a negative sensitivity for bank ratings.

Fitch-rated Sri Lankan banks’ national ratings remain on Rating Watch Negative (RWN) to reflect the potential for the banks’ creditworthiness relative to other entities on the Sri Lankan national ratings scale to deteriorate.

This reflects heightened near-term downside risks to credit profiles from capital and funding stress.

A downgrade of the sovereign’s ‘CC’ Long-Term Local-Currency Issuer Default Rating would not automatically drive a downgrade in Sri Lankan bank ratings. To resolve the RWN on these ratings, we will need to assess the impact to the banks’ capital once debt treatment terms are finalised, including the effects of any present value reductions from an exchange of bonds and those of any regulatory or accounting forbearance. We may resolve and affirm the banks’ ratings if we think risks from funding and capital stresses have abated, at both the individual bank and the sector level, to the extent that we believe the banks’ ability to service obligations in local and foreign currency is not hindered and/or banks are able to continue as a going concern and avoid failure.

Although the government’s domestic debt treatment announcements go some way towards resolving uncertainties over Sri Lankan bank ratings, many risks remain. It is still unclear, for example, whether the government’s proposals have received support from the sovereign’s key external creditors. If not, the risk of further domestic debt restructuring could linger, resulting in further instability for the banking sector.