Rising gold-backed lending among Sri Lanka’s finance and leasing companies (FLC) sector is exposing financiers to higher collateral price risk and making them more susceptible to any adverse movements in gold prices, says Fitch Ratings.

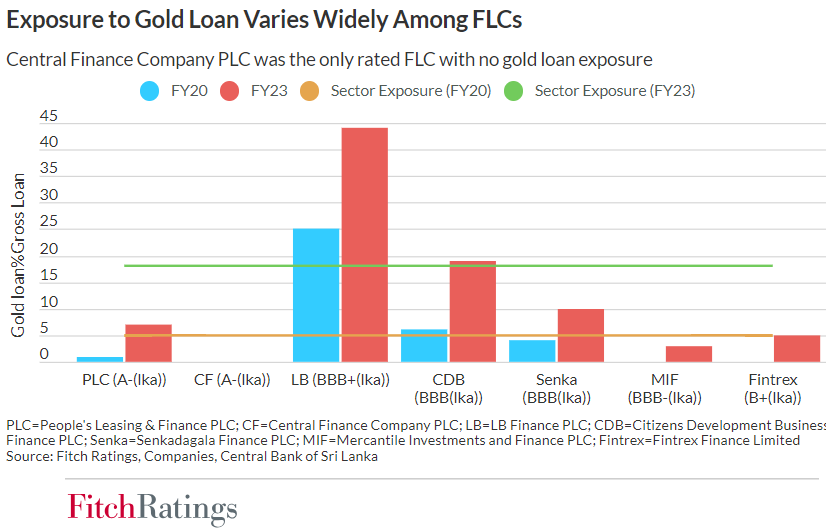

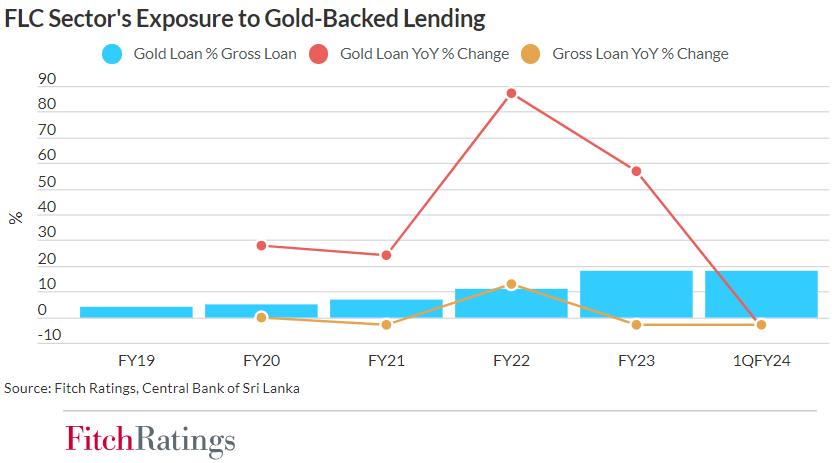

Sri Lankan FLCs have grown gold-backed loans rapidly in the past several years amid shrinking demand for their core vehicle-financing business. Gold-backed loan balances more than quadrupled between the financial year ending March 2019 (FYE19) and FYE23, raising its share in the sector’s gross loans to 18%, from 4% at end-FY19.

We believe several factors have fuelled this trend, including rising demand for shorter-term financing from borrowers, relatively high product yields, and the liquid nature of gold collaterals that allows lenders to recover defaulted facilities through regular auctions. FLCs cut back their exposure to gold-backed lending in 1QFY24, but we view this as temporary, as it stemmed partly from a drop in local gold prices in 1QFY24 following the global price decline, exacerbated by Sri Lankan rupee appreciation during the period.

Excess concentration in gold-backed loans could leave some FLCs prone to large tail risks of devaluations, especially if collateral haircuts are insufficient to protect them from any sudden and precipitous price fall. This was evident in 2012 and 2013 when sharp declines in gold prices drove an increase in non-performing loans (NPLs) and credit costs at many Sri Lankan banks and non-bank financial institutions. Extended loan tenors would leave lenders more exposed to sustained price corrections.

Rising competition among the FLCs has led to an uptick in average loan-to-value (LTV) ratios. They range between 70% and 80% currently but could deteriorate quickly if gold prices fall or borrowers start to default, adding to accrued interest. Gold-backed lending is not subject to any regulatory LTV cap in Sri Lanka, unlike in markets such as India.

The current regulatory capital framework also entices FLCs to build larger gold loan portfolios more quickly than they otherwise would have. It may also cause lenders to underestimate their risk levels and reserve insufficient capital to absorb potential shocks. For instance, gold loans with LTV ratios of up to 70% do not incur any risk weight, and only incremental exposure over the 70% threshold is 100% risk-weighted. This contrasts with India, for example, where gold loans incur the standard 100% risk weight. The drop in local prices in 1QFY24 led to an increase in the risk-weighted share of gold loans to 13%, from 8% in FY23, but we expect this to have mostly reversed in subsequent months as gold prices recovered.

Sri Lankan FLCs do not factor in borrowers’ repayment capacity when underwriting a gold-backed loan, focusing solely on collateral value, like in other markets. Collateral risk mitigation therefore becomes more crucial to protect against losses. However, valuation of gold collaterals is at lenders’ discretion and subject to their own calculation methodologies. The purity of accepted collateral can also vary. This contrasts with markets such as India, where regulators stipulate methods for collateral valuation.

The NPL ratio from Sri Lankan FLCs' gold-backed lending remains well below that of conventional lending products, due mostly to lenders’ ability to recover overdues through frequent gold auctions, and borrowers’ ability to roll over a facility upon maturity by only servicing interest. However, ratios have come under pressure amid the challenging operating environment and borrowers’ weakened repayment capacities. Among Sri Lankan FLCs rated by Fitch based on standalone strength, the 90+ day past-due ratio on gold loans jumped to 5.3% at end-1QFY24, from 1.9% at end-FY22. This is consistent with rising auction volumes, indicating growing defaults in the segment.