By Ashani Abayasekara

The policy proposal in Sri Lanka’s 2021 Budget to impose a 0.25% tax on the revenue of companies to set up a ‘COVID-19 Insurance Fund’ has raised concerns among many private sector industry stakeholders. They argue that this is a big blow to industries already suffering in the wake of the pandemic, and warn that mandating payment of an additional tax can push them to reverse current measures taken to retain staff, amidst dampened business activity and customer demand.

The government’s aim of establishing a guaranteed fund to help workers during COVID-19 and other future crises is well-placed. Statistics from the Department of Census and Statistics show that Sri Lanka’s unemployed population rose by 100,000 during the first quarter of 2020, along with the first countrywide lockdown in March. Increased job losses, however, are often a reflection of enterprise losses too. According to an e-survey conducted by the Department of Labour among a sample of 2,764 private sector organisations, as of May 2020, 53% of the interviewed businesses were closed, and 39% of establishments indicated an inability to pay worker salaries. The means of generating emergency funds, therefore, needs to be thought through carefully for it to be sustainable in the long-run.

While the government – which is grappling with massive debt burdens and fiscal deficits – has limited capacity to assist workers and employers, are there ways in which current employment-related social protection programmes can be used to provide for both job and enterprise protection during crises? What measures have other countries taken that Sri Lanka can learn from? This blog examines these issues.

Current Protection for Private Sector Workers in Sri Lanka

Private sector employees in Sri Lanka are covered by the Employees’ Provident Fund (EPF) and the Employees’ Trust Fund (ETF), both of which provide a lump-sum payment at retirement. Employers and employees contribute jointly to EPF at rates of 12% and 8% of monthly wages, respectively, whereas ETF is financed entirely by employers who are required to contribute 3% of an employee’s salary. Early withdrawals from both funds are only allowed for specific reasons, such as a permanent sickness or disability or permanent migration. There is also limited provision for withdrawal of funds under specified circumstances, such as in cases of economic shocks.

The funds are managed by the Central Bank, and represent the largest source of investments for government domestic borrowing. This means that when the government is cash-crunched, so are the funds.

The active contributions to and usage of the funds have been low due to several reasons, including poor awareness of the schemes and its benefits, and evading or manipulating contribution requirements, given the absence of any near-term benefits and concerns of its sustainability.

As of end 2018, the EPF had a total of 18.6 million accounts, of which only 2.6 million were active, while only 43% of employers contributed to the ETF in 2017.

COVID-19 Policy Responses in Other Countries

The rapid spread of COVID-19 has seen governments across the world resorting to unprecedented measures to support workers and businesses, including income support, investments in healthcare, job retention schemes, and business facilitation. Many developed countries have used already existing unemployment insurance schemes – designed to protect workers against job losses – to extend support. Additionally, countries with provident fund schemes similar to those in Sri Lanka have provided extra benefits and introduced more flexibility.

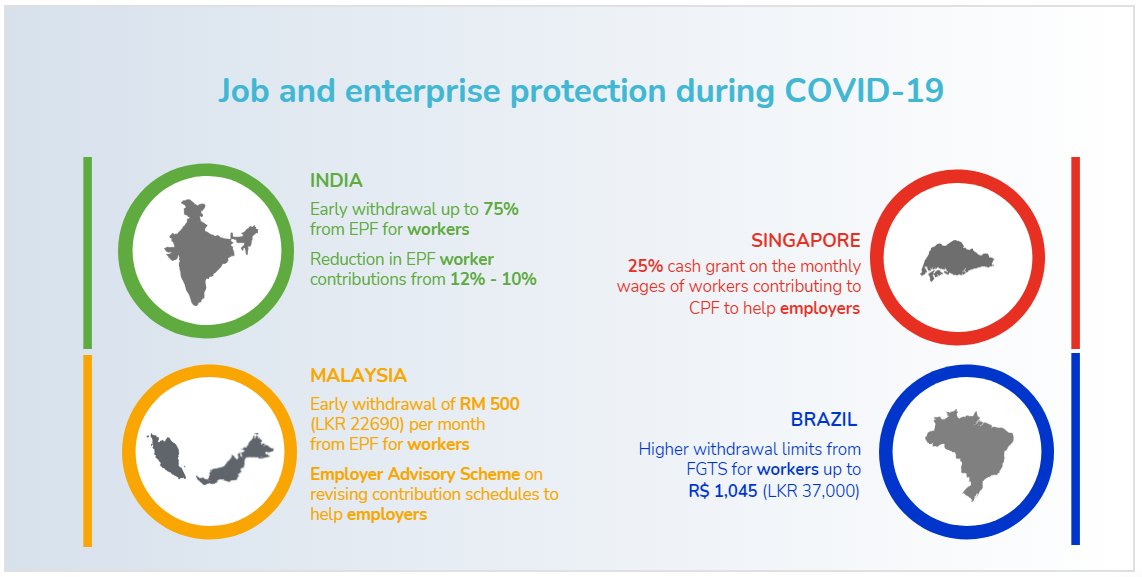

India’s EPF scheme, for example, allows a non-refundable advance when the government has declared a disaster or epidemic, which employees need not deposit back into their EPF account. An amendment to the EPF regulation following COVID-19 now allows employees to withdraw up to 75% of their savings as a non-refundable advance, or three months’ basic salary, whichever is lower. The government also cut employee EPF contributions to 10% from the existing 12% from May-July 2020.

In Malaysia, employees below the age of 55 are allowed to withdraw RM500 (~LKR 22,700) per month from EPF for 12 months, starting March 2020, to buy essential goods. The minimum EPF contribution by employees was reduced from 11% to 7% from 1 April to 31 December 2020, while discussions are also underway to allow certain contributors such as laid-off workers to withdraw funds. To assist employers, an Employer Advisory Scheme was introduced, which evaluates the specific conditions of affected companies and offers tailored plans on EPF contribution schedules, including restructuring or staggering payments for outstanding contributions.

Employers in Singaporeare supported via aJobs Support Scheme, under which they receive a 25% cash grant (up from 8% pre-pandemic) on the monthly wages of each employee who is part of the Central Provident Fund.

In Brazil, the government increased withdrawal limits from theFundo de Garantia por Tempo de Serviço (FGTS) – a fund which provides account-based cash benefits to employees on termination of employment for any reason – up to R$ 1,045 (~LKR 37,000) per worker until December 31 2020, which is expected to benefit over 60 million workers. The FGTS is entirely funded by the employer, via compulsory monthly deposits equivalent to 8% of the employee’s salary.

Looking Ahead

The COVID-19 impacts on Sri Lanka’s labour market have made a strong case for revisiting employment social protection. The country should take this opportunity to introduce reforms to make better use of employment provident funds to support both workers and companies during times of crisis. The above country examples provide important insights in this regard, particularly in allowing for flexible withdrawals from funds in emergencies.

Encouraging more active and regular contributions is essential for there to be sufficient funds to draw from when needed. One option in the current context is to allow withdrawals from ETF – currently funded solely by employers – to provide assistance during the crisis, instead of requiring employers to make additional contributions to a new fund.

Assigning the management and administration of the funds to an independent body is also important to assure a guaranteed return upon retirement or to draw from during emergencies. Creating more awareness of the schemes and different types of benefits they offer will also help encourage more participation.

Ashani Abayasekara is a Research Economist with research interests in labour economics, economics of education, development economics, and microeconometrics. She holds a BA in Economics with First Class Honours from the University of Peradeniya and a Masters in International and Development Economics from the Australian National University. (Talk to Ashani - ashani@ips.lk)