online pharmacy zovirax no prescription

100,500 is 8% at present, but with the new tax regime it will be only 4%.

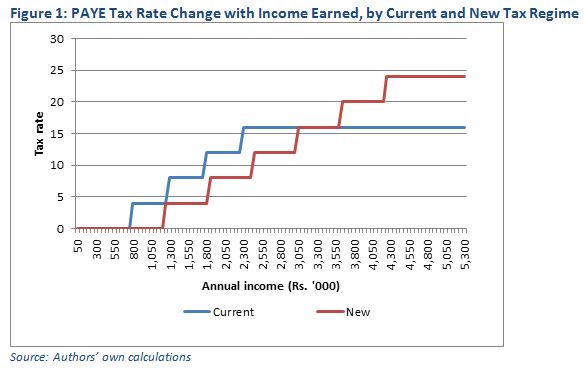

How do these changes to the tax regime affect the payment of taxes?

With the newly-introduced tax regime, less people are required to pay PAYE taxes, due to the tax exempt income threshold being higher. Also, as the tax rates increase at larger income blocks, individuals in the middle income brackets would pay lower taxes than at present. But, because under the new tax regime tax rates will increase beyond 16%, the rich are obliged to pay a higher tax rate than at present (Figure 1).

How do these changes to the tax regime affect the payment of taxes?

With the newly-introduced tax regime, less people are required to pay PAYE taxes, due to the tax exempt income threshold being higher. Also, as the tax rates increase at larger income blocks, individuals in the middle income brackets would pay lower taxes than at present. But, because under the new tax regime tax rates will increase beyond 16%, the rich are obliged to pay a higher tax rate than at present (Figure 1). online pharmacy stromectol no prescription

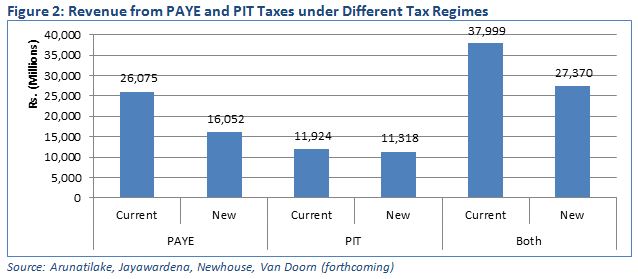

As the tax exempt threshold did not change for PIT taxes, there is no change in the number of individuals required to pay PIT. However, as with PAYE taxes, those in the middle income brackets pay lesser taxes, as the tax rates increase at a slower pace under the new system. How will this affect tax revenue? According to our simulations based on Household Income and Expenditure Survey 2013/14 (HIES) data, the overall revenue from income taxes will decrease due to the proposed tax changes. This is mainly because there is a large revenue drop from lower PAYE taxes. However, it must be noted that the HIES does not capture the income levels of individuals with very high incomes, due to underreporting. Hence, the actual revenue collected may be higher than the estimated value. Although PAYE tax rates will increase for individuals with high incomes (monthly income of more than Rs. 300,000), the number of taxpayers with such high incomes is low. One reason for the decrease in tax revenue is the higher threshold at which individuals are taxed. Although due to the higher threshold less people pay taxes, the new tax regime has also removed concessions (e.g., the earlier tax regime provided a lower tax rate for professionals. Under the new system this has been removed) that are allowed under the current system.

Is the new system more pro-poor?

The new PAYE tax regime is slightly more progressive and income equalizing than the current PAYE tax system. This means, the richer will pay more personal income taxes than the poor. For example, according to our simulations, under the new tax regime, 98% of the revenue from PAYE taxes will come out of the pockets of the richest 30% of Sri Lankans. This is an increase of 3 percentage points from the current tax regime. The increase in the share of PIT paid by the richest 30% of individuals also increases, albeit marginally. Under the new tax regime, 79% of the PIT will be paid by the 30% at the top of the income ladder.

Conclusion

The new tax regime is more income equalizing, as the richest pay a higher share of the taxes. However, if the main objective of the new tax regime is to increase tax revenue, our simulations show that this may not be achieved. On the other hand, along with the changes introduced to the tax regime, the new law eliminates deductions, which can also increase tax revenue

The Inland Revenue Department (IRD) is at present taking measures to improve tax administration to increase tax compliance and collection from high income earners. At present, only a small share of persons in each tax decile is actually paying taxes in Sri Lanka. According to theIRD, as of 2015, just 426,496 employees paid PAYE taxes and only 135,170 individuals paid PIT. If the tax administering process can be improved to net more tax payers, the revenue collected can increase. The share of individuals paying PIT is especially low. According to our estimates, only 2 out 5 required to pay PIT, is actually complying. Therefore, including more people in the tax net can increase the revenue collected.

(Nisha Arunatilake is a Research Fellow and Priyanka Jayawardena is a Research Economist at the Institute of Policy Studies of Sri Lanka)

Is the new system more pro-poor?

The new PAYE tax regime is slightly more progressive and income equalizing than the current PAYE tax system. This means, the richer will pay more personal income taxes than the poor. For example, according to our simulations, under the new tax regime, 98% of the revenue from PAYE taxes will come out of the pockets of the richest 30% of Sri Lankans. This is an increase of 3 percentage points from the current tax regime. The increase in the share of PIT paid by the richest 30% of individuals also increases, albeit marginally. Under the new tax regime, 79% of the PIT will be paid by the 30% at the top of the income ladder.

Conclusion

The new tax regime is more income equalizing, as the richest pay a higher share of the taxes. However, if the main objective of the new tax regime is to increase tax revenue, our simulations show that this may not be achieved. On the other hand, along with the changes introduced to the tax regime, the new law eliminates deductions, which can also increase tax revenue

The Inland Revenue Department (IRD) is at present taking measures to improve tax administration to increase tax compliance and collection from high income earners. At present, only a small share of persons in each tax decile is actually paying taxes in Sri Lanka. According to theIRD, as of 2015, just 426,496 employees paid PAYE taxes and only 135,170 individuals paid PIT. If the tax administering process can be improved to net more tax payers, the revenue collected can increase. The share of individuals paying PIT is especially low. According to our estimates, only 2 out 5 required to pay PIT, is actually complying. Therefore, including more people in the tax net can increase the revenue collected.

(Nisha Arunatilake is a Research Fellow and Priyanka Jayawardena is a Research Economist at the Institute of Policy Studies of Sri Lanka)