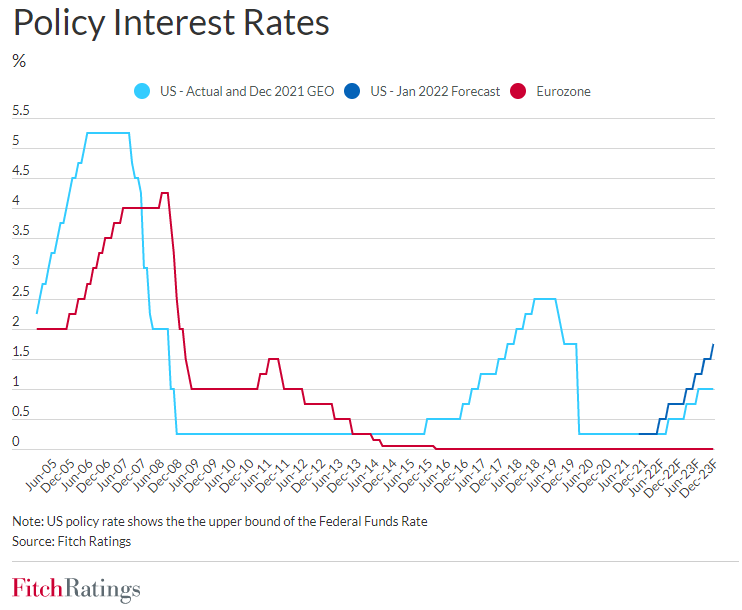

Fitch Ratings expects the Fed to raise rates twice in 2022 and four times in 2023, taking the Fed funds rate (upper bound) to 1.75% by end-2023 from 0.25% currently. Fitch’s updated US interest rate forecasts reflect the major pivot by the Fed at its policy meeting on 14-15 December 2021, prompted by evidence that inflation is broadening and underscored by the meeting minutes.

The previous forecasts (a single 25bp rate rise in 2022 and two in 2023) would have taken the upper bound to 1% at end-2023. These forecasts, published in our Global Economic Outlook on 7 December 2021, pre-dated the Fed’s meeting, in which it signalled that net asset purchases will probably cease in March 2022, and markedly changed its language on inflation.

Most significantly, the Fed described inflation as having exceeded 2% ‘for some time’, suggesting that recent increases have already compensated for earlier shortfalls under the Fed’s flexible average inflation targeting (FAIT) strategy announced in mid-2020. FAIT does not formally define the period over which inflation should average 2%.

The minutes indicate that most Federal Open Market Committee (FOMC) participants think the condition of maximum employment - a criteria for raising rates alongside price stability set under earlier forward guidance - will likely be achieved relatively soon. Also, the Fed is now characterising inflation as a potential threat to a sustained economic recovery and emphasising the need to anchor expectations to avoid sharper policy tightening later on.

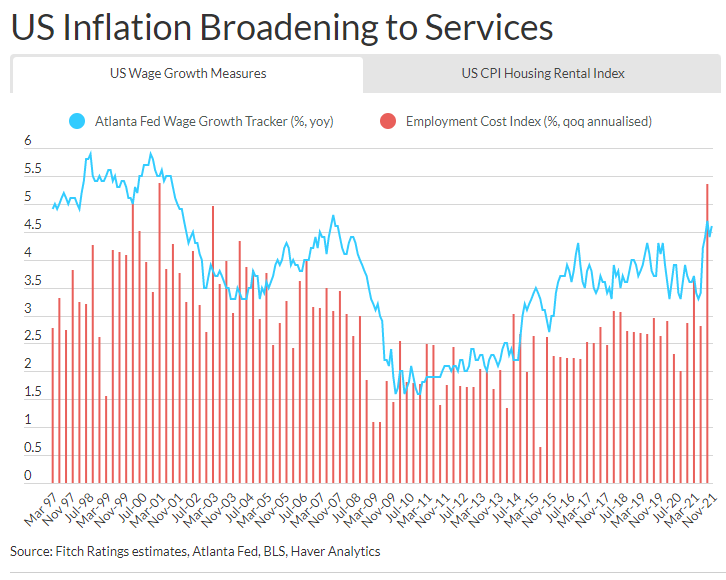

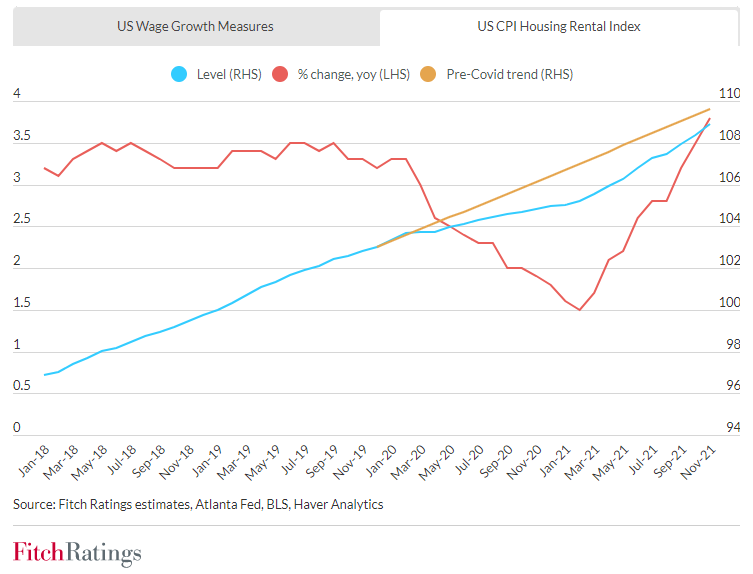

Our previous US policy rate forecasts were already consistent with 2022 being the year in which the Fed’s focus pivoted towards combating inflation risks. Higher-than-expected inflation outturns and rising wage growth and services inflation (including rental inflation) have raised Fed concerns that inflation is broadening beyond the pandemic-related goods price shock, potentially warranting earlier or faster rate rises.

Meanwhile, continuing labor shortages amplify the risk of further increases in wage growth. Recent data showed the US labor force participation rate was unchanged at 61.9% in December 2021, while the unemployment rate had dropped to 3.9%.

We believe this year’s rate rises will come at the Fed’s June and September policy meetings. The omicron variant may delay the advent of maximum employment ahead of the March meeting. Our calculations suggest US payrolls are still about 2 million below this level.

Moreover, the interval between ceasing net asset purchases and raising policy rates will be much shorter than in 2014-2015, but we think the Fed remains committed to predictable sequencing of its policy tightening measures, and will want to monitor financial market reactions after asset purchases are phased out. December’s ‘DOT plot’ showed a median expectation among FOMC members of three rate rises this year, but does not constitute formal forward guidance. The move to unanimity on the need for a rate rise in 2022, from a 50-50 split at September 2021’s policy meeting, was arguably more significant.

Fitch has not changed its US or global GDP forecasts from December’s Global Economic Outlook. We think the private sector is relatively well prepared for higher US borrowing costs, but our updated forecasts reinforce the prospects for higher US Treasury yields and a stronger US dollar against the euro and the Chinese yuan. Despite increases in recent weeks, real yields on inflation-protected bonds remain historically low. We think full normalisation could see US nominal interest rates rise to about 3% over the medium-to-long term, potentially pushing up global rates.

The US economy’s outlook is one of the key topics to be discussed at Fitch Ratings’ Credit Outlook 2022 series, running 12-20 January.