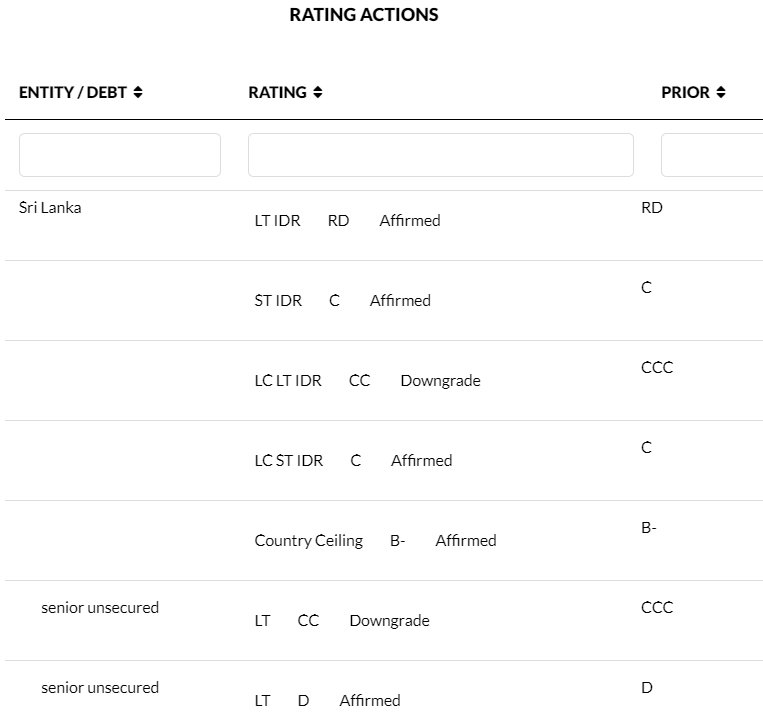

FitchRatings has downgraded Sri Lanka's Long-Term Local-Currency Issuer Default Rating (IDR) to 'CC', from 'CCC', and has affirmed the Long-Term Foreign-Currency IDR at 'RD' (Restricted Default). Fitch typically does not assign Outlooks to ratings of 'CCC+' or below.

Fitch has also removed the Long-Term Local-Currency IDR from Under Criteria Observation, on which it was placed on 14 July 2022, following the publication of the updated Sovereign Rating Criteria.

A full list of rating actions is at the end of this rating action commentary.

KEY RATING DRIVERS

Challenging Domestic Financing Outlook: Sri Lanka continues to service its local-currency debt, but the downgrade of the Long-Term Local-Currency IDR reflects our view that a local-currency debt default is probable, in view of an untenably high domestic interest payment/revenue ratio, high interest costs, tight domestic financing conditions and rising local-currency debt/GDP in the context of high domestic fiscal financing requirements, which authorities forecast at about 8% of GDP in 2022.

According to authorities, domestic interest payments in 8M22 were LKR718.8 billion, taking the domestic interest/revenue ratio to an estimated 56% in 8M22; the highest among sovereigns rated 'CCC+' and below. Reliance on central bank financing has increased, as domestic options are limited. Domestic debt rose to about 53% of government debt by end-July 2022, according to official provisional data. Treasury bill issuance has been increasing. We expect a local debt restructuring would aim to maintain financial system stability, for example, by extending maturities or lowering coupon payments, rather than a reduction in face value. Sri Lanka continues to service its local-currency debt.

External Debt Restructuring: The sovereign remains in default on foreign-currency obligations and has initiated a debt restructuring arrangement with official and private external creditors.The Ministry of Finance issued a statement on 12 April 2022 that it had suspended normal debt servicing of several categories of external debt, including bonds issued in international capital markets, foreign currency-denominated loan agreements and credit facilities with commercial banks and institutional lenders.

Fitch downgraded the Long-Term Foreign-Currency IDR to 'RD' following the expiry of the 30-day grace period on coupon payments that were due on 18 April 2022. A staff level agreement with the IMF was reached on 1 September for USD2.9 billion, for 48 months, under the Extended Fund Facility. The facility will not be approved until Sri Lanka has implemented agreed actions, financing assurances have been received from official creditors and good-faith efforts have been made to reach agreement with private creditors. The timing of completion of the external debt restructuring remains uncertain.

Banking Sector Faces Tight Liquidity: Sri Lankan banks' access to foreign-currency funding is constrained by the sovereign default. Any local-currency debt restructuring would elevate funding and liquidity stress, given the predominance of local-currency funding, at 74% of the total, and large holdings of local currency-denominated government securities. A restructuring could necessitate recapitalisation by the government, though further regulatory forbearance measures could keep banks compliant with regulatory minimums on a reported basis, however, underlying capital positions could stay weak.

Budget Aims for Fiscal Consolidation: In the 2023 budget authorities aim to lower the deficit to 9.8% of GDP in 2022 and 7.9% of GDP in 2023, factoring in high revenue growth and a pickup in spending. It also aims to raise government revenue to 15% of GDP by 2025 and reduce public sector debt to no more than 100% of GDP over the medium term, in line with the IMF's target of a primary surplus of 2.3% of GDP by 2025. We expect a contraction in GDP in 2023 and so are less optimistic on the government's fiscal consolidation path. We expect general government debt/GDP to reach around 109% by end-2022.

Political Risks Weigh on Fiscal Outlook: Political instability could threaten reform implementation. The government's parliamentary position appears strong, but the government lacks public support. This increases the risk of further destabilising protests if economic conditions do not improve or reforms generate public opposition. President Wickremesinghe was prime minister in the previous administration under President Rajapaksa, who was brought down by protests. Parliament and the government also remain dominated by politicians who are affiliated with the Rajapaksa family.

High Inflation: Inflation is high, although it has declined from its September peak of 69.8% as measured by the Colombo Consumer Price Index. We expect headline inflation to fall further in 2023 on easing domestic supply conditions, lower food prices and the impact of policy rate hikes. Risks remain, from a potential commodity-price shock, particularly owing to the war in Ukraine. Financing from the Central Bank has been a key funding source for the government, but a new Central Bank Act, may limit such financing in the future. We believe rate hikes have peaked, after a policy rate hike of 950bp in 2022.

Economy Contracting: Sri Lanka's economy contracted by a sharp 4.8% yoy in 1H22 and we expect a full-year GDP contraction of 6.0%. There is still uncertainty about the pace of the country's economic outlook in 2023, partly because the timing of the external debt restructuring is unknown. We forecast growth to contract by 2.2% in 2023 then to pick up in 2024 under our baseline.

ESG - Governance: Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights as well as for Rule of Law, Institutional and Regulatory Quality and Control of Corruption, as is the case for all sovereigns. This reflects the high weight World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model. Sri Lanka has a medium WBGI ranking in the 46th percentile, reflecting a recent record of peaceful political transitions, and moderate levels of rights for participation in the political process, institutional capacity, established rule of law and a level of corruption.

ESG - Creditor Rights: Sri Lanka has an ESG Relevance Score of '5' for Creditor Rights, as willingness to service and repay debt is highly relevant to the rating and is a key rating driver with a high weight. The downgrade of Sri Lanka's Long-Term Foreign-Currency IDR to 'RD' reflects a default event.

RATING SENSITIVITIES

Factors that could, individually or collectively, lead to negative rating action/downgrade:

- The Long-Term Local-Currency IDR would be further downgraded if the government announces plans to restructure or defaults on its local currency-denominated debt.

Factors that could, individually or collectively, lead to positive rating action/upgrade:

- Completion of a commercial debt restructuring that Fitch judges to have normalised the relationship with private-sector creditors.

- The government puts local-currency debt service on a sustainable path, and avoids a default or debt restructuring.

SOVEREIGN RATING MODEL (SRM) AND QUALITATIVE OVERLAY (QO)

Fitch's proprietary SRM assigns Sri Lanka a score equivalent to a rating of 'CCC+' on the Long-Term Foreign-Currency IDR scale. However, in accordance with its rating criteria, Fitch's sovereign rating committee has not utilised the SRM and QO to explain the ratings in this instance. Ratings of 'CCC+' and below are instead guided by the rating definitions.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a Long-Term Foreign-Currency IDR. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Sovereigns, Public Finance and Infrastructure issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of three notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG CONSIDERATIONS

Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights as WBGIs have the highest weight in Fitch's SRM and are highly relevant to the rating and a key rating driver with a high weight. As Sri Lanka has a percentile rank below 50 for the respective governance indicator, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '5' for Rule of Law, Institutional & Regulatory Quality and Control of Corruption as WBGIs have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight. As Sri Lanka has a percentile rank below 50 for the respective governance indicators, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '4' for Human Rights and Political Freedoms, as the Voice and Accountability pillar of the WBGIs is relevant to the rating and a rating driver. As Sri Lanka has a percentile rank below 50 for the respective governance indicator, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '5' for Creditor Rights as willingness to service and repay debt is highly relevant to the rating and is a key rating driver with a high weight. The downgrade of Sri Lanka's Long-Term Foreign-Currency IDR to 'RD' reflects a default event.

Except for the matters discussed above, the highest level of ESG credit relevance, if present, is a score of 3. This means ESG issues are credit-neutral or have only a minimal credit impact on the entity(ies), either due to their nature or to the way in which they are being managed by the entity(ies).