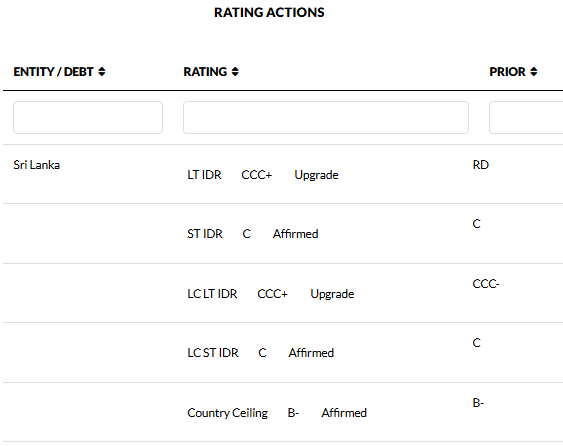

Fitch Ratings has upgraded Sri Lanka's Long-Term Foreign-Currency Issuer Default Rating (IDR) to 'CCC+', from 'RD' (Restricted Default). Fitch typically does not assign an Outlook to sovereigns with a rating of 'CCC+' or below.

Fitch has also upgraded the Local-Currency IDR to 'CCC+', from 'CCC-', to align with the Long-Term Foreign-Currency IDR, as the risk of another default on local-currency debt has been reduced by the completion of the international sovereign bond restructuring and an improved outlook for macroeconomic indicators. Sri Lanka completed the local-currency portion of its domestic debt optimisation in September 2023, following the exchange of treasury bills and provisional advances held by Central Bank of Sri Lanka's into new treasury bonds and bills.

A full list of rating actions is at the end of this rating action commentary.

Key Rating Drivers

Foreign-Currency Debt Exchange: The upgrade of the Long-Term Foreign-Currency IDR reflects Fitch's assessment that Sri Lanka has normalised relations with a majority of creditors, after the announcement of final results of the invitation to exchange the outstanding stock of international sovereign bonds with a 98% participation rate. One bond series with non-aggregated collective action clauses did not meet the required 75% level. Without this bond series, the acceptance results imply a restructuring of 96% of total commercial external debt.

New Debt Instruments: The debt exchange will convert 11 international sovereign bonds and accumulated past due interest (PDI) into a mix of four macro-linked bonds, one governance-linked bond and one PDI bond. Bondholders can choose the local alternative governed by domestic law, with rupee-denominated bonds and a US dollar bond with step-up coupon payments.

Other Commercial and Official Debt Restructuring: Sri Lanka is also restructuring debt to commercial and official creditors. An agreement in principle has been reached with most commercial creditors including international banks for an amount of about USD200 million. Restructuring of debt owed to official creditors is expected to be completed by end-2024.

Improved External Finances: Sri Lanka's foreign-currency debt restructuring offers substantial upfront debt repayment relief, with no foreign-currency bond maturities until 2029. The first amortisation on the macro-linked bonds, which have low coupon rates until 2032, starts from 2029. Governance linked bond amortisation begins in 2034 and the US-dollar step-up bonds start amortisation in 2029. We expect foreign-exchange reserves to reach USD8.7 billion by 2026, also reflecting debt relief over the period.

Debt Still High: The debt restructuring has reduced the government's debt service burden and liquidity risks, but general government debt/GDP and the interest/revenue ratio are likely to stay high in the medium term. The restructuring under Fitch's baseline assumptions lowers general government debt/GDP to about 90% by 2028, while Fitch forecasts the interest/revenue ratio to decline to 42%, still well above the 'CCC' median of 16%. This is, however, a large drop from the 67% in 2021, prior to the sovereign default.

Fiscal Reform Challenging: Sri Lanka has a weak long-term revenue raising record, but the government implemented several major tax measures to boost revenue collection and achieve debt sustainability. Fitch expects general government revenue/GDP to exceed 15% by 2026, from 11% in 2023, broadly in line with IMF programme projections. Downside risks could be substantial if the government fails to raise revenue.

Strong Mandate from Election Outcome: Sri Lanka's September 2024 presidential election was won by a leader of the opposition National People's Power, which secured over two-thirds majority in the legislature. Fitch expects the new government to support progress on reforms. The new government has said it will continue to implement the 48-month IMF extended fund facility, which began in March 2023. Sri Lanka has made major progress on the programme under the previous government.

Economy Recovering: Sri Lanka's economy is recovering after a contraction in 2022 and 2023. In seasonally adjusted terms, real GDP growth in 3Q24 recovered to 5.2%, after contracting by 7.4% in 2022 and 2.2% in 2023. This was driven by an 11.1% pick-up in industrial growth, while services grew by about 2.8%. We expect growth to recover to 4.1% in 2024 and average 3.6% over 2025-2026.

Inflation in Check: The Central Bank's policy measures have largely reversed a rise in inflation, which peaked in September 2022 at 67.2% (seasonally adjusted). Inflation continues to decline, falling to -2.1% yoy in November 2024. The central bank has eased monetary policy significantly, reducing the standing deposit facility rate by a cumulative 800 bp since June 2023. Fitch expects further easing over 2025-2026, in line with its expectation that underlying inflationary pressure will remain muted and the central bank will meet its medium-term inflation target of 5.0%.

Banking Sector Improving: Economic reforms implemented since the crisis period have improved headline macroeconomic metrics, reduced systemic risks and support banks' operating flexibility. Asset quality stress has peaked and declining credit costs are driving higher profitability. Pressure on foreign- and local-currency funding and liquidity has eased on better external flows and banks' efforts to preserve liquidity. Fitch expects banks to regain access to foreign-currency wholesale funding, following the restoration of the sovereign's creditworthiness.

ESG - Governance: Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights as well as for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. These scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in Fitch's proprietary Sovereign Rating Model (SRM). Sri Lanka has a medium WBGI ranking in the 38th percentile, reflecting a recent record of peaceful political transitions, a moderate level of rights for participation in the political process, moderate institutional capacity, established rule of law and a moderate level of corruption.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

-Public Finances: An increase in government debt/GDP, potentially reflecting an inability to further raise revenue, resulting in wider budget deficits.

- External Finances: Inability to rebuild foreign-exchange reserves that weakens debt repayment capacity.

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

- Public Finances: A sustained decline in the general government debt/GDP ratio that is underpinned by strong implementation of a credible medium-term fiscal consolidation strategy, increase in fiscal revenue and faster economic growth.

Fitch's proprietary SRM assigns Sri Lanka a score equivalent to a rating of 'CCC+' on the Long-Term Foreign-Currency IDR scale. In accordance with the rating criteria for ratings in the 'CCC' range and below, Fitch has not used the SRM or QO to explain the ratings, which are instead guided by Fitch's rating definitions.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a Long-Term Foreign-Currency IDR. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

Country Ceiling

The Country Ceiling for Sri Lanka is affirmed at 'B-'. Fitch assumes a starting point of 'CCC+' to determine the Country Ceiling for sovereigns rated 'CCC+' and below. Fitch's Country Ceiling Model produced a starting point uplift of zero notches above the IDR. Fitch applied a +1 notch qualitative adjustment to the model result, under the balance of payments restrictions pillar. The Country Ceiling reflects Fitch's view that the private sector has not been prevented or significantly impeded from converting local currency into foreign currency and transferring the proceeds to non-resident creditors to service debt.

Fitch does not assign Country Ceilings below 'CCC+' and only assigns a Country Ceiling of 'CCC+' in the event that transfer and convertibility risk has materialised and is affecting the vast majority of economic sectors and asset classes.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG Considerations

Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights, as WBGI have the highest weight in Fitch's SRM and are highly relevant to the rating and a key rating driver with a high weight. As Sri Lanka has a percentile rank below 50 for the respective governance indicator, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '5' for Rule of Law, Institutional & Regulatory Quality and Control of Corruption, as WBGI have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight. As Sri Lanka has a percentile rank below 50 for the respective governance indicators, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '4' for Human Rights and Political Freedoms, as the Voice and Accountability pillar of the WBGI is relevant to the rating and a rating driver. As Sri Lanka has a percentile rank below 50 for the respective governance indicator, this has a negative impact on the credit profile.

Sri Lanka has an ESG Relevance Score of '4' for Creditor Rights, as willingness to service and repay debt is highly relevant to the rating and is a key rating driver with a high weight. As Sri Lanka had a recent event of default on public debt in 2022, this has a negative impact on the credit profile.

The highest level of ESG credit relevance is a score of '3', unless otherwise disclosed in this section. A score of '3' means ESG issues are credit-neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. Fitch's ESG Relevance Scores are not inputs in the rating process; they are an observation on the relevance and materiality of ESG factors in the rating decision.